{kind=link}

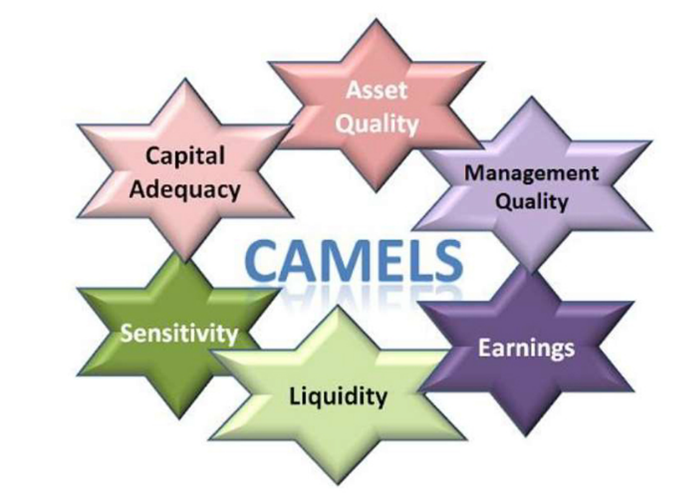

In operations management, “CAMELS” refers to a rating system used by bank supervisory authorities to assess the financial health of financial institutions, focusing on six key areas: Capital Adequacy, Asset Quality, Management, Earnings, Liquidity, and Sensitivity to Market Risk. In India the banks supervisory authority is Reserve Bank of India.

C: The capital adequacy ratio (CAR) is a measure of how much capital a bank has available, reported as a percentage of a bank’s risk-weighted credit exposures. The purpose is to establish that banks have enough capital on reserve to handle a certain number of losses, before being at risk for becoming insolvent. For Indian banks, the Reserve Bank of India (RBI) mandates a Capital Adequacy Ratio (CAR) of at least 9% for scheduled commercial banks and 12% for public sector banks.

A: Asset quality refers to the assessment of the credit risk associated with an asset, particularly in the context of bank loans and investments. It essentially evaluates how likely an asset is to generate the expected return and avoid losses.

M: Bank management involves the strategic oversight and administration of all banking activities, encompassing areas like regulatory compliance, operational efficiency, risk management, customer service, and financial product development, all with the goal of maximizing profitability.

E: Earning banks generally earn money by borrowing money from depositors and compensating them with a certain interest rate. The banks will lend the money out to borrowers, charging the borrowers a higher interest rate and profiting off the interest rate spread.

L & S: A bank’s liquidity & sensitivity refers to its ability to meet short-term obligations, while sensitivity to market risk refers to how its earnings and asset values change with market fluctuations, impacting its overall stability.

CAMELS rating system is on a scale of one to five, with one being the best rating and five being the worst rating. One of the research projects titled “A Study of CAMELS Performance of Bank of Baroda and HDFC Bank” conducted by Kumar and Singh in 2023 examines into an analysis comparing two prominent banks, in India, namely Bank of Baroda and HDFC Bank. The study utilized the CAMEL’s framework to assess their performance. The Indian banking industry plays a fundamental role in the nation’s economic development and financial stability. Ensuring that the health and strength of the banks operating in this dynamic environment and market is of paramount importance. This research dives into the comprehensive assessment framework known as CAMEL’s model.

To analyse the performance and the reliability of the banking institutions operating within the Indian Banking Sector. The study employs a multi-layered approach, combing quantitative and qualitative methodologies to determine the strength of the weakness of the Banks. It examines the chief components of C.A.M.E.L.S and their impact on stability and resilience of bank, providing an understanding of the criteria used by investors and the regulatory authorities to evaluate the health of banking institutions. Through a review of Banks financial statements and empirical data, this research paper sheds light on the Indian Banking Industry which is continuously changing landscape. The research also tried to understand how effectively the CAMEL framework addresses the emerging challenges, potential risk, and vulnerabilities within the sector. Furthermore, this paper discussed the importance of CAMELS in assessments on decision-making processes of investors and bank management. Many Ratios metrics and analysis were made that will support the CAMEL’s model.

Bank of Baroda is India’s second largest public sector bank which has not only established a strong presence domestically but also internationally. It was founded in 1908. BOB boasts a history filled with reliability, innovation, and customer focus. The bank offers a range of products and services to cater to individuals and businesses of all sizes. With a customer base exceeding 128 million worldwide and operations across 24 countries with over 100 branches and offices Bank of Baroda has positioned itself as a strong player. What distinguishes Bank of Baroda is its role in banking serving, over 70 million users through mobile banking. Bank of Baroda has gained the trust of families in India because of its financial performance, global presence, and dedication, to digital advancements.

HDFC Bank, the private sector bank, in India has a total business volume of over INR 25 trillion and a global customer base of more than 100 million. They have a network of ATMs with over 19,000 machines making it one of the largest in India. Additionally, HDFC Bank is at the forefront of mobile banking services. It serves than 50 million customers through their innovative mobile banking solutions. In terms of market capitalization, it holds the position among banks. With its reach and inventive solutions HDFC Bank continues to set standards for excellence in banking. This study aims to analyse the performance of two banks within their respective sectors: Bank of Baroda, a public sector bank and HDFC Bank, as a private sector bank. The analysis has utilized C.A.M.E.L.s model a research tool to evaluate the health of both organizations. The CAMELS model is widely used to evaluate the wellbeing of banks and credit unions.

Regulators rely on this model to assess the safety and stability of institutions by assigning ratings from 1 to 5 for each component. The Reserve Bank primarily supervise banking sector like a hawk in India. While India experienced some impact from the 2008 global financial crisis, the Reserve Bank of India (RBI) and the Indian government’s proactive measures helped mitigate its effects, preventing a full-blown crisis like in other countries. A rating like CAMELS helps regulators identify areas of concern and take actions for improvement. Ultimately the CAMELS model serves as a tool to ensure that institutions maintain capital effectively manage risks generate sustainable earnings and fulfil their obligations. Additionally, ratio analysis is employed alongside the CAMELS model to identify strengths and weaknesses, within organizations.

Based on CAMEL analysis, the best banks in India for 2025 are HDFC Bank, ICICI Bank, State Bank of India (SBI), Kotak Mahindra Bank, and Axis Bank. These banks are recognized for their strong financial stability, customer service, and range of banking services.