Credit Rating Agencies have been around since a long time since early 19th century in USA. They have played an important role in the financial world by providing ratings on the creditworthiness of bonds and other debt instruments. Rating agencies play a vital role in fixing interest rates on debt securities. The idea of using services of rating agencies to assess the level of risk associated with a debt took place around the beginning of the 20th century.

The issuers of the securities such as companies, special purpose entities or sovereign governments which issue government bonds, corporate bonds, CD (Certificate of deposit), municipal bond, preferred stocks, and collateralized securities, such as mortgage backed securities and collateral debt are rated based on their financial health by the rating agencies. The ratings have an effect on the interest rates that a security pays out, while higher ratings lead to lower interest rates. Individual consumers are rated for creditworthiness not by credit rating agencies but by credit bureaus which are also called consumer reporting agencies or credit reference agencies, which issue credit scores.

entities or sovereign governments which issue government bonds, corporate bonds, CD (Certificate of deposit), municipal bond, preferred stocks, and collateralized securities, such as mortgage backed securities and collateral debt are rated based on their financial health by the rating agencies. The ratings have an effect on the interest rates that a security pays out, while higher ratings lead to lower interest rates. Individual consumers are rated for creditworthiness not by credit rating agencies but by credit bureaus which are also called consumer reporting agencies or credit reference agencies, which issue credit scores.

Trustworthiness questioned: On the flipside, the value of credit ratings for securities has been extensively questioned, as hundreds of billions of securities that were given the agencies’ highest ratings were downgraded to junk during the financial crisis of 2007-08. Also, rating downgrades during the European sovereign debt crisis of 2010–12 were blamed by EU officials for adding to the crisis. The rating agencies also go wrong sometimes. Some economists feel that they are given excessive importance.

Since 2011, the independent rating companies have had to obtain certification from the European Securities and Market Authority (ESMA) in order to operate in Europe. ESMA performs regular inspections to ensure that the rating agencies are following European regulations and the authority can issue sanctions for any infractions.

Operating charges: Credit rating agencies collect a fee either from the entity seeking to receive a rating (business or government) or from the entity seeking to use and analyze the rating (the financial analysis department of a bank, financial institution, etc.).

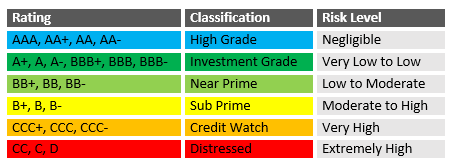

Modes Operandi: To assess the solvency of borrowers, rating agencies issue credit ratings related to the credit risk represented by the borrower, or in other words, the risk that the borrower will default on the loan. Credit ratings place this risk on a scale ranging from low risk (investment category) to high risk (speculative category). Although there is no standard scale, credit ratings are typically expressed by letters corresponding to the potential risk, with the highest rating symbolized by AAA and the lowest rating by C or D, according to the agency. In addition to the letter grade, a credit rating might also consist of a “forecast” that describes how a particular rating may change in the future. For example, a credit rating with a negative position may indicate a future downgrade.

Each rating agency uses its own method to calculate its ratings. These methods take into account quantitative (financial data), qualitative data such as business strategy of a company or political stability for a country and related criteria such as changes in industry for a company or public finances for a country. The final rating represents the credit agency’s evaluation of a borrower’s credit risk at a given time. It does not comprise investment advice.

Importance of credit ratings: Along with other criteria, investors take credit ratings into account to help manage their portfolios. A rating downgrade indicates a greater risk for the lender. Depending on the sensitivity of the market, investors may require a higher return to protect against this risk, which in turn raises financing costs for the borrower. Many investors give credit ratings a lot of importance while taking their investment decisions. This is how credit rating agencies play a big role in financial markets. Banks are also evaluated by credit rating agencies. One such bank is BNP Paribas which has received higher credit ratings by Fitch and Standard & Poor.

Globalization gave push to the agencies: Globalization gave an impetus to the financial markets in both investments and debts coupled with diversification in the types and quantities of securities issued. This presents a challenge to institutional and individual investors who need to be analyzed on the risks associated with both foreign and domestic investments.

The Big Three: Fitch Ratings, Moody’s Investors Service and Standard & Poor’s.

John Knowles Fitch founded the Fitch Publishing Company in 1913. Fitch published financial statistics for use in the investment industry via “The Fitch Stock and Bond Manual” and published “The Fitch Bond Book.” In 1924, Fitch introduced the AAA through D rating system that has become the basis for ratings throughout the industry. With plans to become a full-service global rating agency, in the late 1990s Fitch merged with IBCA of London, subsidiary of Fimalac, S.A., a French holding company. Fitch also acquired market competitors Thomson BankWatch and Duff & Phelps Credit Ratings Co. Beginning in 2004, Fitch began to develop operating subsidiaries specializing in enterprise risk management, data services and finance industry training with the acquisition of Canadian company, Algorithmic, and the creation of Fitch Solutions and Fitch Training.

Moody’s Investors Service: John Moody and Company first published “Moody’s Manual” in 1900. The manual published basic statistics and general information about stocks and bonds of various industries. From 1903 until the stock market crash of 1907, “Moody’s Manual” was a national publication. In 1909 Moody began publishing “Moody’s Analyses of Railroad Investments”, which added analytical information about the value of securities. Expanding this idea led to the 1914 creation of Moody’s Investors Service, which, in the following 10 years, provided ratings for nearly all of the government bond market at the time. By the 1970s Moody’s began rating commercial paper and bank deposits, becoming the full-scale rating agency that it is today.

Standard & Poor’s: Henry Varnum Poor first published the “History of Railroads and Canals in the United States” in 1860, the forerunner of securities analysis and reporting to be developed over the next century. Standard Statistics formed in 1906, which published corporate bond, sovereign bond, and municipal bond ratings. Standard Statistics merged with Poor’s Publishing in 1941 to form Standard & Poor’s Corporation, which was acquired by The McGraw-Hill Companies, Inc. in 1966. Standard and Poor’s has become best known by indexes such as the S&P 500, a stock market index that is both a tool for investor analysis and decision making, and a U.S. economic indicator.

In India, CIBIL, CRISIL and ICRA are the leading three agencies.

CIBIL (Credit Information Bureau India Limited) its main objectives are to track the credit history of an individual or a company and rate their creditworthiness. The CIBIL scores are used by lending organizations to sanction loans quickly and for the approval of credit cards too. Their rating scales vary between 350 and 900. Generally, a rating of above 700 is considered positive. A high credit score allows consumers to avail all types of loans easily and at good interest rates.

CRISIL (Credit Rating Information Services of India Limited) International rating agency Standard & Poor’s (S&P) has become the majority shareholder of CRISIL in 2005 with 49.7 per cent stake. CRISIL’s main objectives are to establish the creditworthiness of companies based on the business strengths, the board of directors, the market share, and reputation of the company and so on. CRISIL rates organization like public limited companies, banks and financial organizations and not individuals. CRISIL ratings help investors to obtain a clear idea about an organization before investing in their debentures and bonds. CRISIL offers 8 different grades credit scoring. They are CRISIL AAA, CRISIL AA, CRISIL A – The three grades offer maximum safety for timely servicing of the loans. CRISIL BBB, CRISIL BB Offer moderate safety. CRISIL B, CRISIL C, CRISIL D suggests High-risk individuals.

ICRA (Investment Information and Credit Rating Agency of India) It offers 12 types of ratings which include, Corporate debt rating, Financial sector rating, Issuer rating, Bank loan credit rating, Public finance rating, Corporate governance rating, Structured finance rating, SME rating, Mutual fund rating, Infrastructure sector rating, Project finance rating and Insurance sector rating, ICRA is known for its comprehensive ratings offered through a transparent rating system. The ICRA rating system includes symbols that represent the ability of a corporate entity to service its debt obligations in a timely manner. The rating symbols vary with the financial instruments considered.

{kind=link}