Risk Management in Banking

{kind=link}

It is always advisable to be ready for global financial crisis and for sound and comprehensive risk governance. Board members and senior executives of banks need to have an inclusive view of risk control and far-reaching value creation. They must be clear on how risk categories are interconnected to the economy, capital allocation and the value of the business.

A risk is defined as an unplanned event with financial consequences resulting in loss or reduced earnings. Therefore, a risky proposition is one with looming loss. Risk stems from uncertainty or unpredictability of the future. In a commercial venture risk generates profit or loss depending upon the way in which it is managed. Risk can be defined as the instability of the potential outcome. Risk is the possibility of something adverse happening.

Risk management is the process of evaluating risk, taking steps to reduce risk to tolerable level. Thus, we can say that after the risks are identified, risk management attempts to lessen their effects. For example, we buy insurance to lessen financial risks. Also, sometimes when people visualize too many hurdles in a project, they re-plan the whole project.

Following are some common risks occurring in the banking industry:

Credit Risk: The main risk under this category is the risk of non recovery of loan and the risk of lessening in the value of asset. Banks face credit risk when customers repay loans by making the pre-payment, thus resulting in loss of opportunity to the bank to earn higher interest income. When banks give huge amount of loans to a single borrower, or to a single industry or to a single city, state or country risk arises due excess exposure. In regards to excess loans given in a country, the element of country risk arises due to losses in foreign exchange reserve or unfavorable political or economic situations in the country or its neighboring country.

While the definition of credit risk sounds simple and straight forward, measuring it is not so simple. Some examples are poor or falling cash flow from operations which is often needed to make the interest and principal payments, rising interest rates, changes in the nature of the marketplace such as a change in technology, an increase in competitors, or regulatory changes. The credit risk associated with foreign bonds also includes the home country’s sociopolitical situation and the stability and regulatory practices of its government. Rating agencies like Moody’s and Standard & Poor’s analyze credit risks on various securities.

Interest Rate Risk: This risk arises due to fluctuations in the interest rates. It can result in reduction in the revenues of the bank due to fluctuations in the interest rates which are dynamic and which change differently for assets and liabilities. Interest rates are market determined and banks have to fall in line with the market trends even though it may suppress their Net Interest margins. Interest rates depend of economic growth (demand and supply of money) fiscal policy (in a booming economy, many firms need to borrow funds to expand their plants, finance inventories and even acquire other firms). Consumers might be buying cars and houses. That need keeps the demand for capital at a high level and interest rates higher than they otherwise might be) monetary policy (Central banks modify the money supply to try to manage the economy and control inflation. If a government loosens monetary policy, this means that it has “created more money”) another key factor for rate fluctuation is inflation. Investors try to preserve their “purchasing power,” during period of high inflation as they get higher interest rate on their investments in the shortest period of time.

Liquidity Risk: Liquidity is the ability to meet commitments as and when they are due and ability to undertake new transactions when they are profitable. Liquidity risk may derive due to net outflow of funds arising out of withdrawals, non renewal of deposits, non-recovery of cash receipts from recovery of loans, conversion of contingent liabilities into fund based commitment and increased sanctioned limits.

Foreign Exchange Risk: Banks face risk which arises due to foreign exchange. Foreign Exchange risk arises when a bank holds assets or liabilities in foreign currencies and impacts the earnings and capital of bank due to the fluctuations in the exchange rates. No one can predict what the exchange rate will be in the next period, it can move in either upward or downward direction regardless of what the estimates and predictions were. This uncertain movement poses a threat to the earnings and capital of bank, if such a movement is in undesired and unforeseen direction. Foreign Exchange Risk can be either Transactional or it can be Translational. When the exchange rate changes unfavorably it give rise to Transactional Risk, as the name implies because of transactions in Foreign Currencies, can be evaded

using different techniques. Other one Translational Risk is an accounting risk

arising because of the translation of the assets held in foreign currency or abroad.

Regulatory Risks: Regulatory risk is the risk of a change in regulations and law that might affect the banking industry/ a particular sector. Such changes in regulations can make significant changes in the framework of an industry, changes in some clause regarding lending etc. Change in laws and regulations materially impact a security, business, sector or market. When a change is made in law or regulations made by the government or a regulatory body it can increase the costs of operating by banks; it immediately affects the depositor’s and borrower’s behavior. It reduces attractiveness of investments and also changes the competitive landscape.

Technology Risk: This risk is associated with computers and the communication technology which is being increasingly introduced in the banks. Banks face risk of obsolescence and the risk of losing business to technologically strong financial institutions. A global survey conducted by Deloitte Touche Tohmatsu Limited (DTTL) confirms that there are big challenges on the operational risk and technology side such as cyber threats. The acceleration of speed in the capital markets and overall risk management issues, are bothering the financial institutions such as banks. Technology or operations risk software; technology risk is often lumped under the label “operational risk.”

Market Risk: This is the risk of losses in off and on balance sheet positions arising from movements in market prices.

Strategic Risk: This is the risk arising out of certain strategic decisions taken by a bank for sustaining itself in the present day scenario for example decision to open a subsidiary may run the risk of losses if the subsidiary does not do good business.

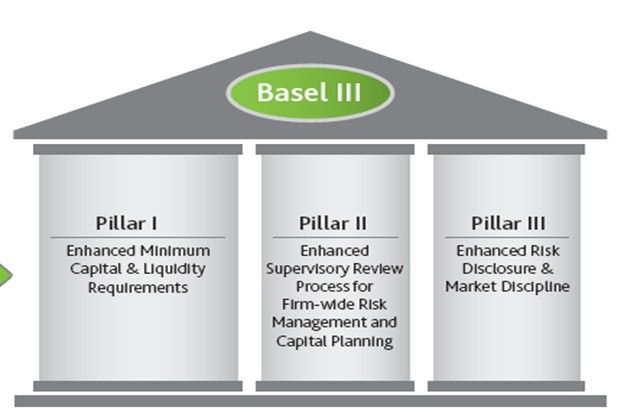

“Basel III” is a comprehensive set of reform measures in banking prudential regulation developed by the Basel Committee on Banking Supervision to strengthen the regulation, supervision and risk management of the banking sector. The measures aim at improving the banking sector’s ability to absorb shocks arising from financial and economic stress, whatever the source may be, to improve risk management and governance and to strengthen banks’ transparency and disclosures. Basel III has provided a framework for stricter and better capital quality, risk coverage, measures to promote the build-up of capital that is unseen in periods of crisis or boom. Secondly, it introduced the ratio of leverage (>=3%) and reconsider the raking system. These changes aim to raise banks’ capability of facing systemic shocks due to economic crisis.